Europe is serious about becoming the first continent to become climate neutral. This is demonstrated by the increasing rules and regulations in the area of sustainability. In order to maintain an overview and not get bogged down in the details, property professionals need to know the interrelationships and effects of the most important directives.

From seasonal shopping to electric vehicles; sustainable considerations are now part of everyday life in large parts of Europe. This change is particularly impressive in the investment business: more and more people want to invest their money sustainably. In Germany alone, the investment volume of sustainable mutual and investment funds has increased twenty-fold in ten years to around 262,3 billion euro in 2023.

This is entirely in the interests of the European Union. After all, sustainable finance is the key to mobilising the necessary investments for the transition to a climate-neutral economy, as envisaged by the Green Deal. Various packages of measures and regulations will ensure that more capital flows into sustainable projects and companies in the future.

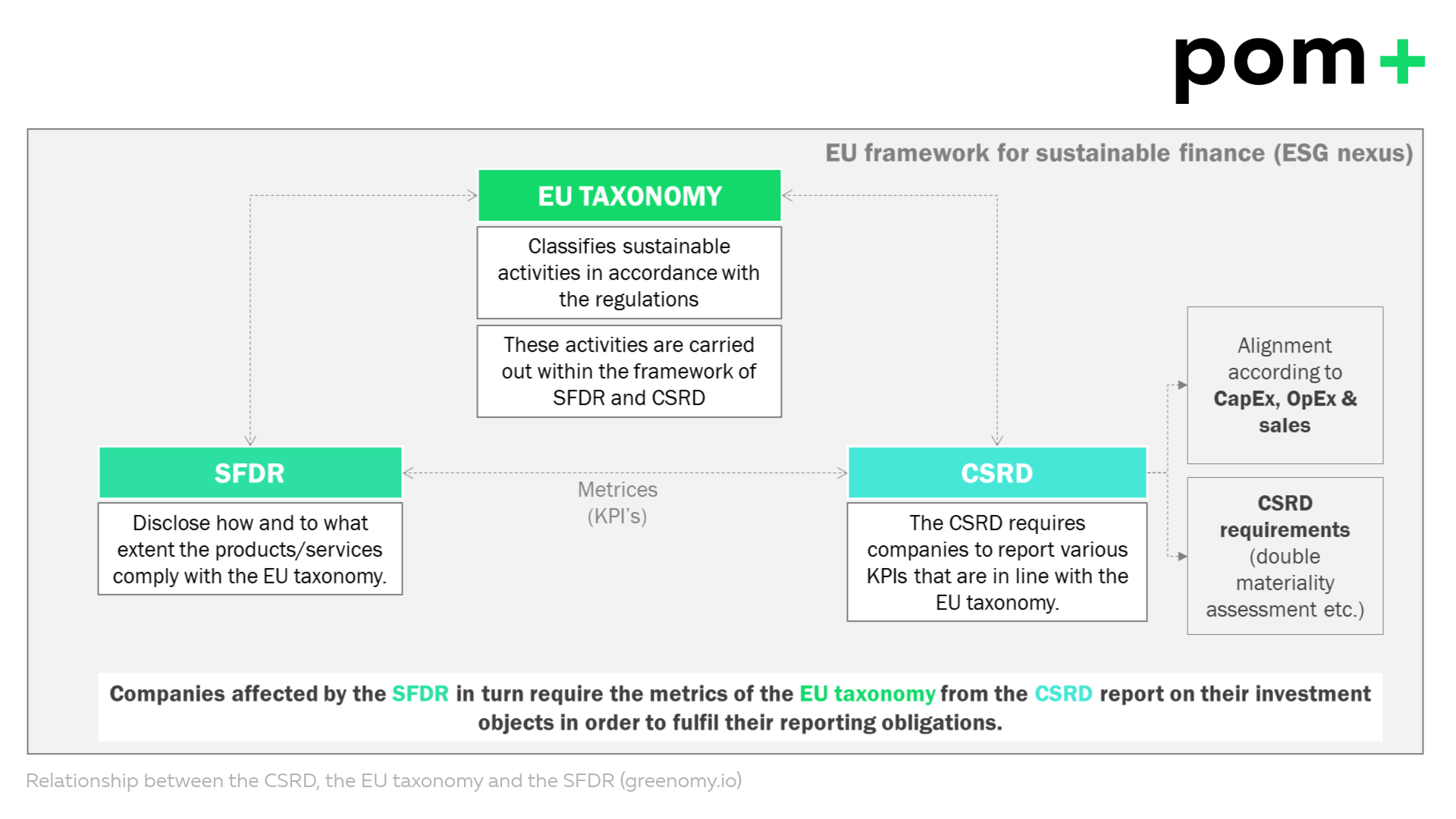

It is therefore crucial for professional property investors, portfolio holders and asset managers to understand the complicated web of regulations and the interrelationships. The EU taxonomy, the Corporate Sustainability Reporting Directive (CSRD) and the Sustainable Finance Disclosure Regulation (SFDR) form the backbone of the European agenda to combat climate change and promote sustainable finance.

{kind=link}

The EU taxonomy: a classification system for sustainability

The centrepiece of the EU sustainability strategy is the EU taxonomy. This is a classification system with criteria for environmentally sustainable economic activities. It forms the regulatory framework for channelling investments into sustainable projects.

For the property sector, the acquisition and ownership of properties, the construction of new buildings and the installation of energy-efficient technologies are particularly important in this context. Ultimately, the aim is to ensure that investments contribute to one or more of the six environmental objectives and do not significantly compromise the other objectives.

The objectives of the EU taxonomy are:

- mitigation of climate change

- adaptation to climate change

- sustainable use and protection of water and marine resources

- transition to a circular economy

- prevention and control of pollution

- protection and restoration of biodiversity and ecosystems

The objectives of the EU taxonomy are broadly defined and the assessment of target fulfilment leaves a certain amount of room for interpretation. This is where the Corporate Sustainability Reporting Directive (CSRD) comes in. It contributes to the comparability of reporting by obliging companies to record and report sustainable measures in a standardised manner.

From 2026, companies must publish CSRD-compliant reports retroactively to the previous year if they fulfil two of the following criteria: a balance sheet total of at least 25 million euros, a net turnover of more than 50 million euros or more than 250 employees. The CSRD also applies to non-European companies that generate a net turnover of more than 150 million euros in the EU and have at least one local subsidiary or branch.

The directive stipulates that companies must provide both qualitative and quantitative data on their sustainability practices, including both historical information and future targets. The required key performance indicators (KPIs) are aligned with the EU Taxonomy Regulation (Article 8).

The data to be provided includes, among other things:

- Direct emissions (Scope 1)

- Indirect emissions from energy consumption (Scope 2)

- Other indirect emissions along the value chain (Scope 3)

- Share of renewable energy

- Pollutant emissions to air, water and soil

However, various other aspects must also be disclosed with regard to the scope of the sustainability strategy in the company, the proportion of women in management positions, the composition and diversity of the Board of Directors, the processes for incorporating sustainability aspects into strategic decisions or the costs of environmental measures and compliance.

This makes it a sticking point for property investors, asset managers and portfolio holders, but above all for CREM organisations, as the required data is often not available at all in the real estate sector, or if it is, then only sparsely. As a result, information from various data sources often has to be tapped, merged, plausibilised and interpreted in order to comply with reporting obligations.

SFDR: Nachhaltige Finanzierung vorantreiben

Finally, the Sustainable Finance Disclosure Regulation supplements the EU taxonomy and the CSRD by setting out binding disclosure requirements for financial market participants. The regulation aims to increase transparency about how sustainability risks are integrated into investment decisions.

For property professionals, the SFDR requires disclosure of sustainability risks and the potential negative impact of investment decisions on sustainability factors. This regulation requires asset managers to align their reporting with the taxonomy's technical screening criteria to ensure that their investments are truly sustainable.

Effects on real estate

The interplay between the EU taxonomy, CSRD and SFDR creates a comprehensive regulatory framework that should drive the property sector as a whole towards greater sustainability. In particular, the focus is on harmonising standards: The CSRD and SFDR require property organisations to use the EU Taxonomy criteria to report on their sustainability performance.

This has a direct impact on the technological environment. Property companies must implement robust data management systems to meet the detailed reporting requirements of the CSRD. This includes collecting accurate data on energy consumption, emissions and other sustainability metrics, which are also essential for SFDR compliance.

To navigate this regulatory environment, property investors and asset managers should:

- Invest in technologies that facilitate real-time data collection and centralisation of sustainability metrics

- Develop standardised procedures for data validation and reporting to meet CSRD requirements

- Review their investment or property portfolios and align with EU taxonomy criteria where necessary to ensure compliance with CSRD (e.g. using sustainability labels at building level)

Getting the ball rolling: First steps

The EU taxonomy, the CSRD and the SFDR jointly aim to create a transparent and sustainable financial system. Conversely, for the property sector this means that comprehensive data management, strict reporting standards and sustainable investment strategies must be introduced.

Pragmatism is now required! Instead of being overwhelmed by this charter, it is worth simply getting started. Ideally with the CSRD, because time is of the essence. In the initial setup, we recommend placing more emphasis on continuous learning and adaptation than on perfection. Specifically: Tailor the objectives to your own organisation, record current and planned measures and define suitable metrics and indicators. Where these parameters are still missing, improvements can be made before the next reporting year.

We are happy to provide support.